Introduction: The Indian Dividend Landscape

India’s dividend culture has evolved significantly over the decades, reflecting the country’s economic transformation, regulatory changes, and corporate governance improvements. From traditionally conservative payout policies to increasingly shareholder-friendly approaches, Indian companies offer unique insights into dividend dynamics in an emerging market context.

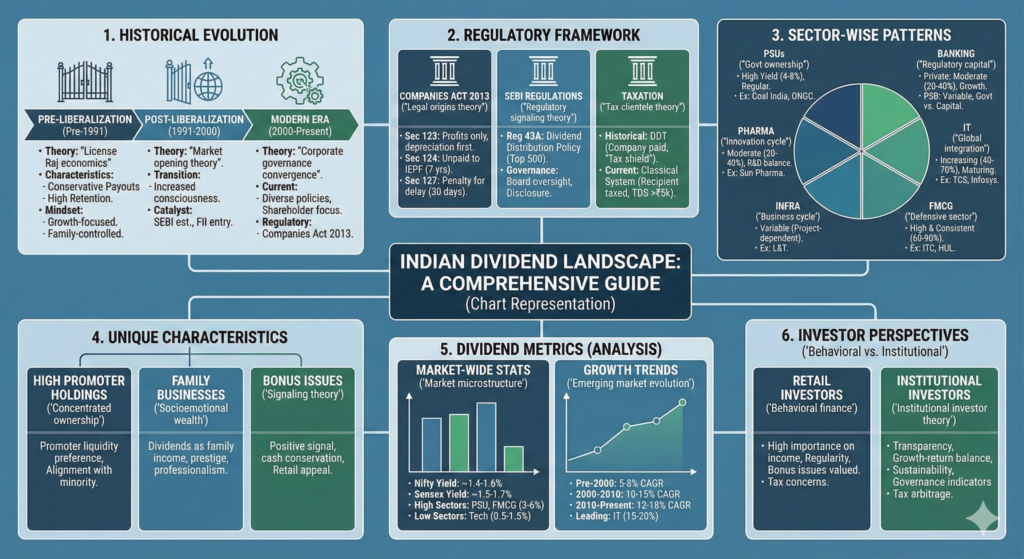

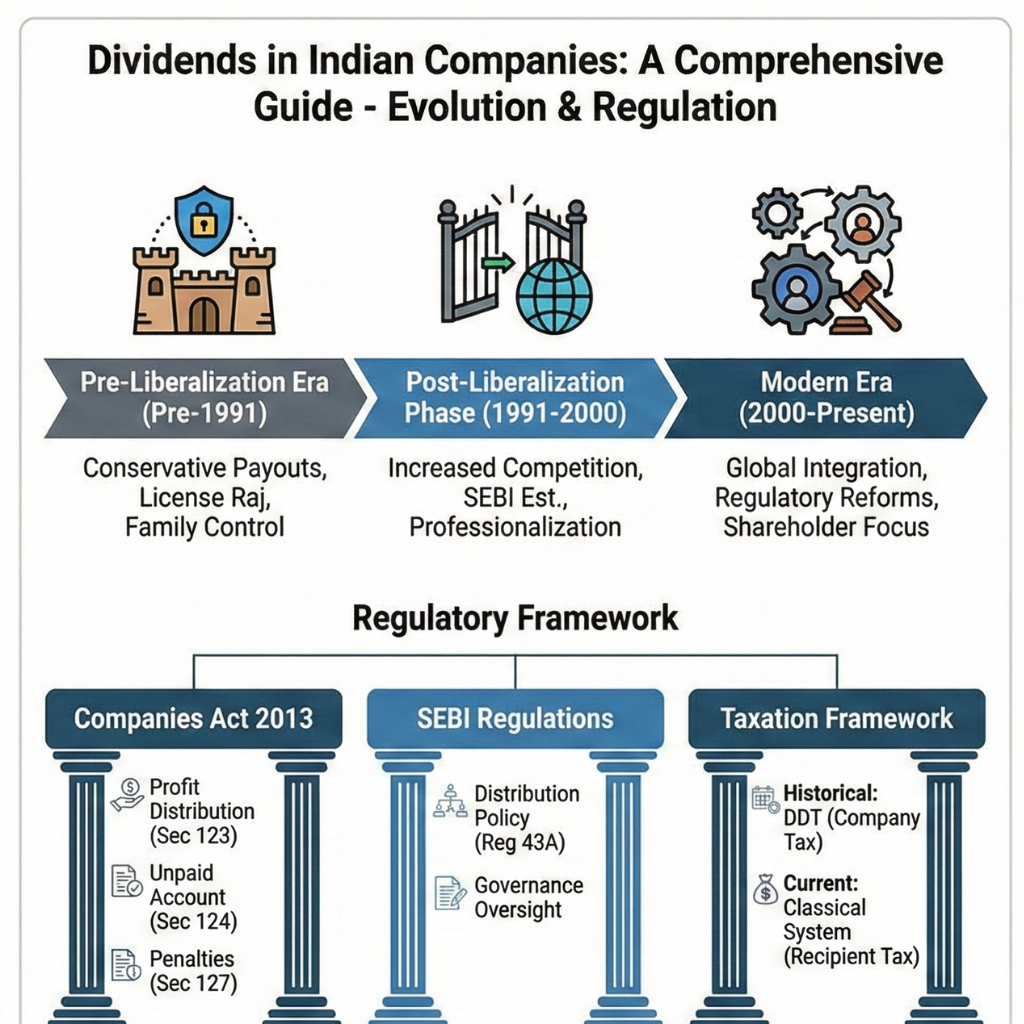

📜 Historical Evolution of Dividend Culture in India

Pre-Liberalization Era (Pre-1991)

Theoretical Insight: ‘License Raj economics’ created protected markets with limited competition, allowing companies to retain earnings for expansion in a capital-scarce economy, resulting in conservative dividend policies.

Characteristics: Low dividend payouts, high retention ratios

Regulatory Environment: Strict capital controls, limited foreign investment

Corporate Mindset: Growth-focused, family-controlled businesses prioritizing expansion

Examples: Traditional family businesses like Tata, Birla groups

Post-Liberalization Phase (1991-2000)

Theoretical Insight: ‘Market opening theory’ suggests that increased competition and access to global capital markets forced Indian companies to adopt more shareholder-friendly policies to attract foreign investment.

Transition: Gradual increase in dividend consciousness

Catalyst: SEBI establishment (1992), foreign institutional investors entry

Change: Professionalization of management, improved governance

Impact: Beginning of regular dividend cultures in professionally managed companies

Modern Era (2000-Present)

Theoretical Insight: ‘Corporate governance convergence theory’ explains how global integration and regulatory reforms (Clause 49, Companies Act 2013) have aligned Indian dividend practices with international standards.

Current State: Diverse dividend policies across sectors

Regulatory Framework: Companies Act 2013, SEBI LODR regulations

Investor Expectations: Increasing demand for shareholder returns

Trend: Balance between growth reinvestment and dividend distribution

🏛️ Regulatory Framework Governing Indian Dividends

Companies Act 2013 Provisions

Theoretical Basis: ‘Legal origins theory’ applied to India shows how common law heritage provides strong minority shareholder protection, mandating equitable distribution of profits.

Section 123: Declaration of Dividend

Only out of profits for the year or previous years

Depreciation must be provided before dividend declaration

Transfer to reserves may be required in certain cases

Section 124: Unpaid Dividend Account

Unclaimed dividends for 7 years transferred to Investor Education and Protection Fund

Ensures proper accounting and prevents misuse

Section 127: Penalty for Failure to Distribute

Directors liable if dividend declared but not paid within 30 days

Demonstrates legal seriousness of dividend commitments

SEBI Regulations

Theoretical Insight: ‘Regulatory signaling theory’ suggests that SEBI’s dividend distribution guidelines serve as corporate governance markers, influencing investor perceptions and company valuations.

Dividend Distribution Policy (Regulation 43A)

Top 500 listed companies must formulate dividend policy

Policy must be disclosed on website and in annual report

Parameters must include circumstances for non-payment

Corporate Governance Requirements

Board and audit committee oversight of dividend decisions

Disclosure of utilization of retained earnings

Transparency in related-party transactions affecting profits

Taxation Framework

Theoretical Perspective: ‘Tax clientele theory’ explains how India’s shifting dividend taxation regime (from DDT to classical system) has altered investor preferences and corporate payout decisions.

Historical: Dividend Distribution Tax (DDT)

Company paid tax on distributed dividends (until 2020)

Created “tax shield” effect for shareholders

Simplified tax collection but distorted payout decisions

Current: Classical System (2020 onward)

Dividends taxed in hands of recipients

TDS applicable above ₹5,000 threshold

Aligns with global practices, increases transparency

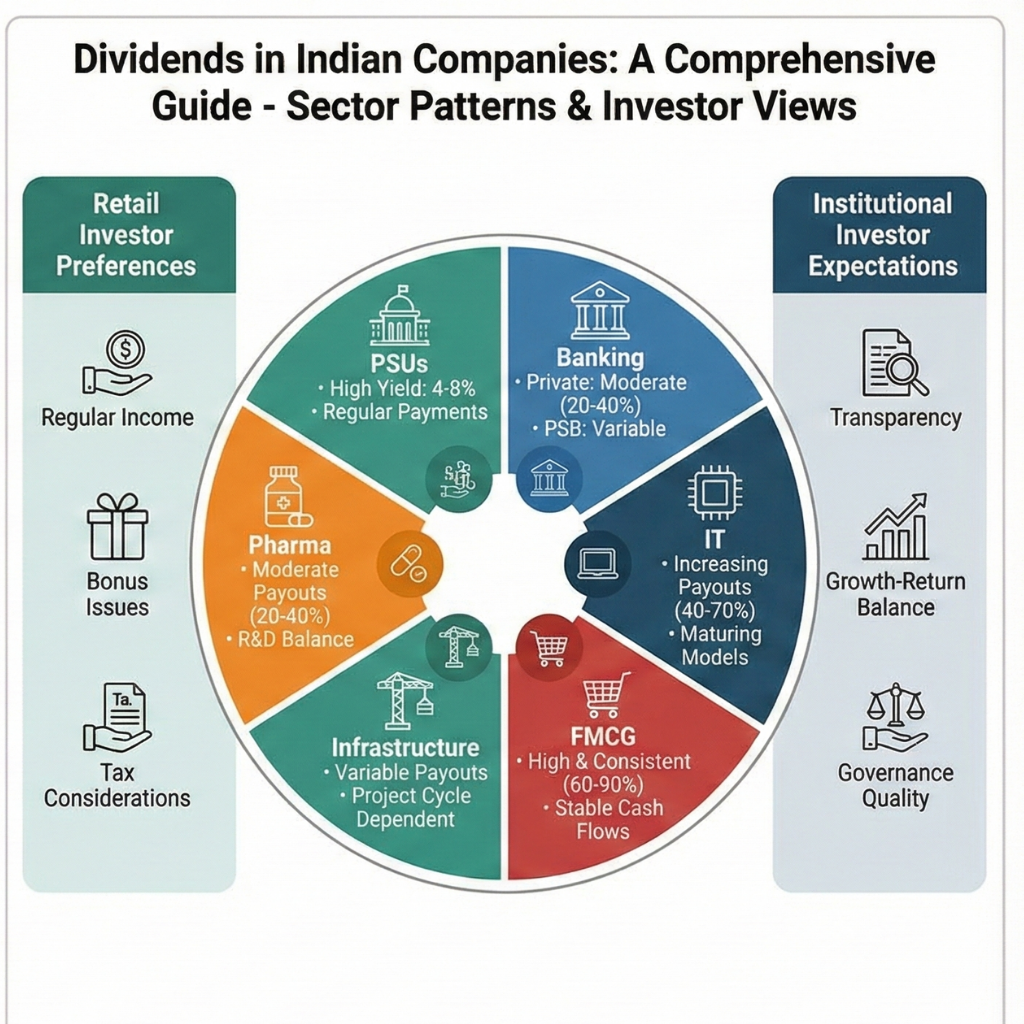

📊 Sector-Wise Dividend Patterns in India

1. Public Sector Undertakings (PSUs)

Theoretical Insight: ‘Government ownership theory’ suggests PSU dividends serve dual purposes: providing shareholder returns to government and functioning as quasi-fiscal tools for resource mobilization.

Characteristics:

High Dividend Yield: Often 4-8% range

Regular Payments: Government pressure for consistent dividends

Examples: Coal India (5-7%), ONGC (4-6%), Power Grid (4-5%)

Rationale: Cash-rich operations, limited growth capital requirements

Unique Aspect: Dividends supplement government revenues

2. Banking & Financial Services

Theoretical Insight: ‘Regulatory capital theory’ explains how RBI’s capital adequacy requirements (Basel norms) create cyclical dividend patterns, with payouts increasing during strong capital position periods.

Private Banks:

Moderate Payouts: 20-40% typically

Growth Focus: Reinvestment for expansion

Examples: HDFC Bank (30-35%), ICICI Bank (20-25%)

Constraints: Regulatory capital requirements, NPA cycles

Public Sector Banks:

Variable Payouts: Government dividend expectations vs. capital needs

Examples: SBI (25-40% depending on performance)

Challenges: Balancing regulatory capital, government expectations, growth needs

3. Information Technology

Theoretical Insight: ‘Global integration theory’ shows how Indian IT companies’ dividend policies reflect their position in global value chains, balancing offshore cash reserves with domestic shareholder expectations.*

Characteristics:

Increasing Payouts: Maturing business models

Payout Ratios: 40-70% range

Examples: TCS (80-100%), Infosys (70-85%), Wipro (40-50%)

Trend: Transition from growth to value phase

Unique: Large offshore cash balances affecting dividend decisions

4. Fast Moving Consumer Goods (FMCG)

Theoretical Insight: ‘Defensive sector theory’ explains FMCG’s high dividend consistency through stable demand patterns, pricing power, and limited cyclicality, creating reliable cash flows for distribution.

Characteristics:

High & Consistent: Regular dividend increases

Payout Ratios: 60-90% typically

Examples: ITC (80-85%), HUL (90-95%), Nestle India (70-80%)

Rationale: Stable cash flows, mature markets, brand dominance

Quality Marker: Dividend consistency reflects business stability

5. Infrastructure & Capital Goods

Theoretical Insight: ‘Business cycle theory’ applied to infrastructure explains variable dividend patterns tied to project cycles, regulatory approvals, and capital expenditure requirements.

Characteristics:

Variable Payouts: Project cycle dependent

Examples: L&T (30-50%), UltraTech Cement (20-40%)

Challenges: Large working capital needs, long gestation projects

Pattern: Lower during expansion phases, higher during maturity

6. Pharmaceuticals

Theoretical Insight: ‘Innovation cycle theory’ shows how R&D intensity and patent cliffs create dividend policy tensions between funding future innovation and rewarding current shareholders.

Characteristics:

Moderate Payouts: 20-40% range

Examples: Sun Pharma (20-30%), Dr Reddy’s (20-25%)

Balance: R&D funding needs vs. shareholder returns

Trend: Increasing as businesses mature

💰 Unique Indian Dividend Characteristics

High Promoter Holdings Impact

Theoretical Insight: ‘Concentrated ownership’ theory explains how high promoter stakes in Indian companies create dividend preferences aligned with promoter needs, including tax planning and liquidity requirements.

Effects:

Promoters often prefer dividends over buybacks for personal liquidity

Dividend policies may reflect promoter cash flow needs

Alignment between promoter and minority shareholder interests in dividend expectations

Dividend Culture in Family Businesses

Theoretical Insight: ‘Socioemotional wealth theory’ applied to Indian family businesses shows how dividends serve both financial and non-financial purposes, including family prestige, intergenerational wealth transfer, and reputation management.

Patterns:

Traditional conservative approach giving way to regular payouts

Dividends as family income source while maintaining control

Increasing professionalism in dividend decisions

Bonus Issues Tradition

Theoretical Insight: Signaling theory in Indian context suggests bonus issues serve as positive signals about future prospects while conserving cash, particularly appealing in a market with strong retail investor participation.

Unique Aspect:

Indian companies frequently issue bonus shares alongside dividends

Psychological appeal to retail investors

Combines reward with capital base expansion

📈 Dividend Metrics: Indian Context Analysis

Market-Wide Statistics

Theoretical Basis: ‘Market microstructure’ theory applied to dividends examines how India’s unique investor composition (high retail participation) affects dividend yield patterns and market reactions to dividend announcements.*

Current Averages:

Nifty 50 Dividend Yield: ~1.4-1.6%

Sensex Dividend Yield: ~1.5-1.7%

Historical Range: 1.2-2.5% depending on market cycles

Sector Variations:

Highest Yields: PSUs, FMCG, Utilities (3-6%)

Lowest Yields: Technology, Consumer Discretionary (0.5-1.5%)

Dividend Growth Trends

Theoretical Perspective: ‘Emerging market dividend evolution theory’ tracks how Indian companies’ dividend growth rates reflect economic development stages and corporate maturity progression.

Historical Growth:

Pre-2000: 5-8% CAGR

2000-2010: 10-15% CAGR

2010-Present: 12-18% CAGR (with sector variations)

Leading Sectors:

IT Services: Highest dividend growth (15-20% CAGR)

Private Banks: Moderate growth (10-15% CAGR)

FMCG: Steady growth (8-12% CAGR)

🎯 Investor Perspectives: Indian Market Realities

Retail Investor Preferences

Theoretical Insight: ‘Behavioral finance theory’ explains Indian retail investors’ strong dividend preference through mental accounting, income illusion, and cultural factors favoring regular returns.

Characteristics:

High importance placed on dividend income

Preference for regular, predictable payments

Bonus issues particularly valued

Tax considerations increasingly important

Institutional Investor Expectations

Theoretical Framework: ‘Institutional investor theory’ shows how FIIs and domestic institutions use dividend policies as governance indicators, preferring companies with clear, consistent payout frameworks.

Preferences:

Transparency in dividend policy

Balance between growth and returns

Sustainability of payouts

Governance quality indicators

Tax Implications for Different Investors

Theoretical Application: ‘Tax arbitrage theory’ explains how India’s dividend taxation changes have created shifting advantages for different investor categories, influencing portfolio decisions.

Current Tax Structure:

Individuals: Taxable as income, TDS above ₹5,000

Corporate Investors: Dividend income taxable, but deduction available

Foreign Investors: Subject to treaty benefits, typically lower rates

Comparison: Dividends vs. capital gains tax efficiency